Has Google lately turned up the visibility dial for “manufacturers”?

Each consulting pitch deck has a “construct a powerful model” slide. Everyone knows “model” is necessary for web optimization.

We’ve all heard Eric Schmidt’s quote: “Manufacturers are the answer, not the issue. Manufacturers are the way you type out the cesspool.”

The influence of branding is just not unique to web optimization. The entire business of brand name advertising and marketing exists as a result of shoppers search out manufacturers they belief.

However Schmidt’s quote dropped in 2008 (when customers have been apparently simply as annoyed with internet outcomes as at present). Again then, Google didn’t perceive content material in addition to at present and leaned rather more on consumer and fundamental backlink indicators.

In the present day, the natural search panorama seems very totally different:

So, have “manufacturers” gained? The reply is sure, however solely in some verticals. However what even defines a model?

Definition

Within the context of web optimization, I outline a “model” as a site that will get:

- Vital model search quantity.

- Larger than anticipated CTR.

- A data card.

- Excessive model recall/NPS.

- Rising variety of model key phrases.

- A significant variety of related backlinks with model anchor textual content.

The best way it would materialize in Search:

- Manufacturers see larger than common conversion charges as a result of customers belief manufacturers extra.

- Customers seek for model mixture key phrases, like “shopify model title generator”

- It’s seemingly that model indicators outweigh different indicators as huge manufacturers get away with extra.

Google provides manufacturers preferential therapy as a result of:

- Customers need them. Schmidt mentioned in the identical interview concerning the cesspool: “Model affinity is clearly laborious wired. It’s so basic to human existence that it’s not going away. It will need to have a genetic part.”

- Aggregators will be intermediaries, which is much less useful for searchers (assume meta-search engines).

- Google competes with extra aggregators head-on (assume Amazon/retailers).

The implications for SEO Aggregators will be extreme.

In David vs. Goliath, I analyzed the highest 1,000 winner and loser websites over the past 12 months and located that “larger websites certainly develop sooner than smaller websites, however seemingly not as a result of they’re huge however as a result of they’ve discovered development levers they’ll pull over a very long time interval.”

Essential: “ecommerce retailers and publishers have misplaced essentially the most,” whereas manufacturers like Lenovo, Sigma, Coleman, or Hanes gained visibility, as I known as out within the follow-up article.

Digging deeper right into a set of just about 10,000 key phrases I monitor within the Semrush Enterprise Suite, we will see a shift in some verticals over the past 12 months.

Journey: extra manufacturers

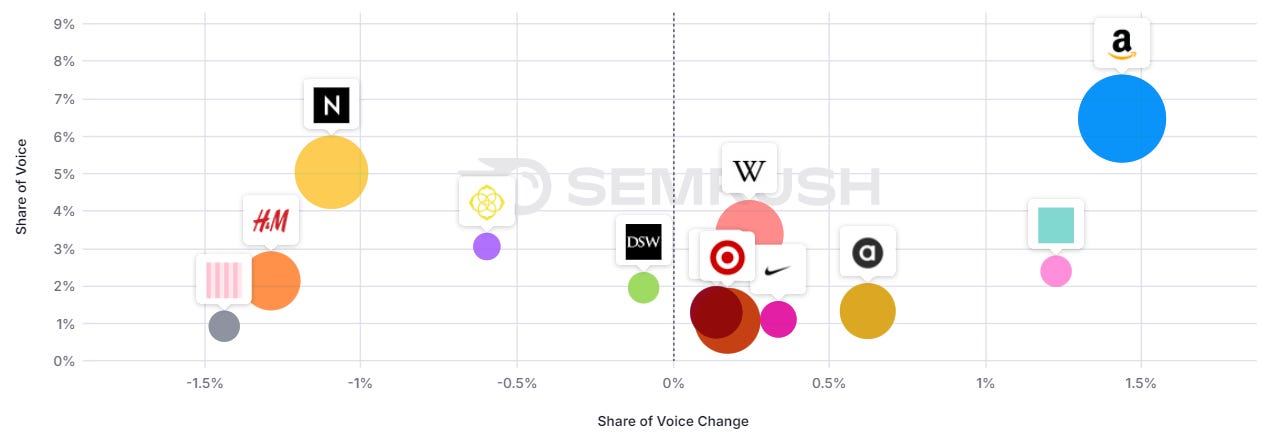

Vogue: combined image

Picture Credit score: Kevin Indig

Picture Credit score: Kevin IndigBeds: combined image

Picture Credit score: Kevin Indig

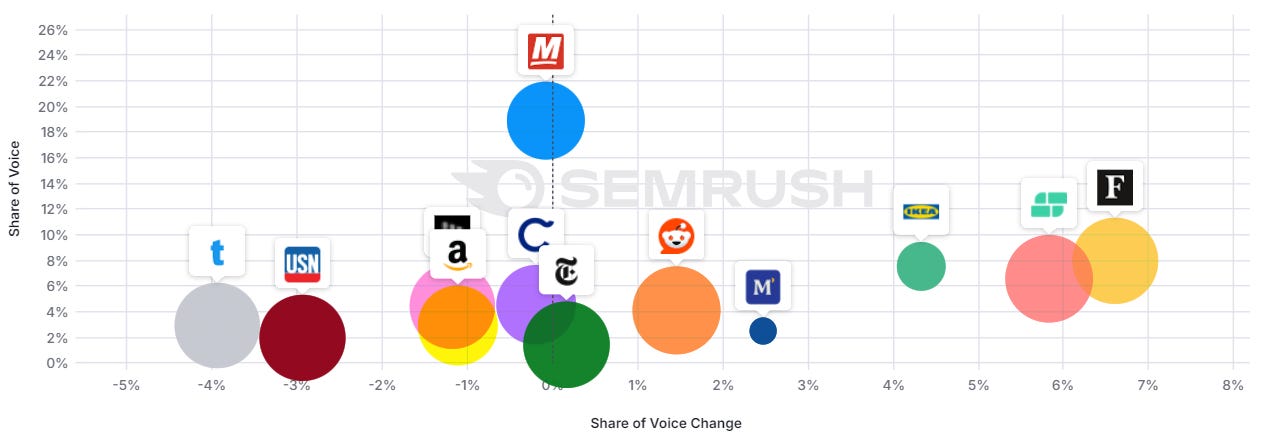

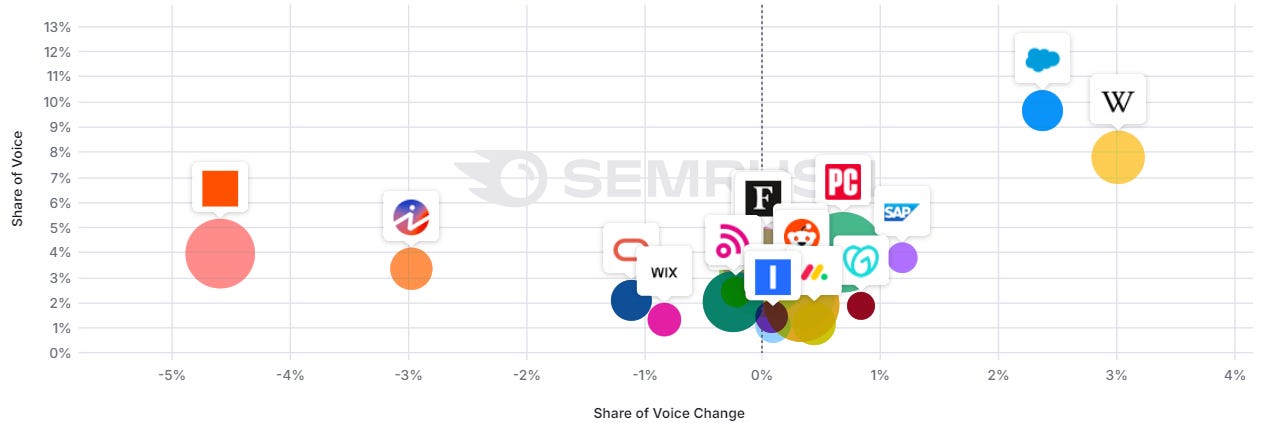

Picture Credit score: Kevin IndigFinance: extra manufacturers

Picture Credit score: Kevin Indig

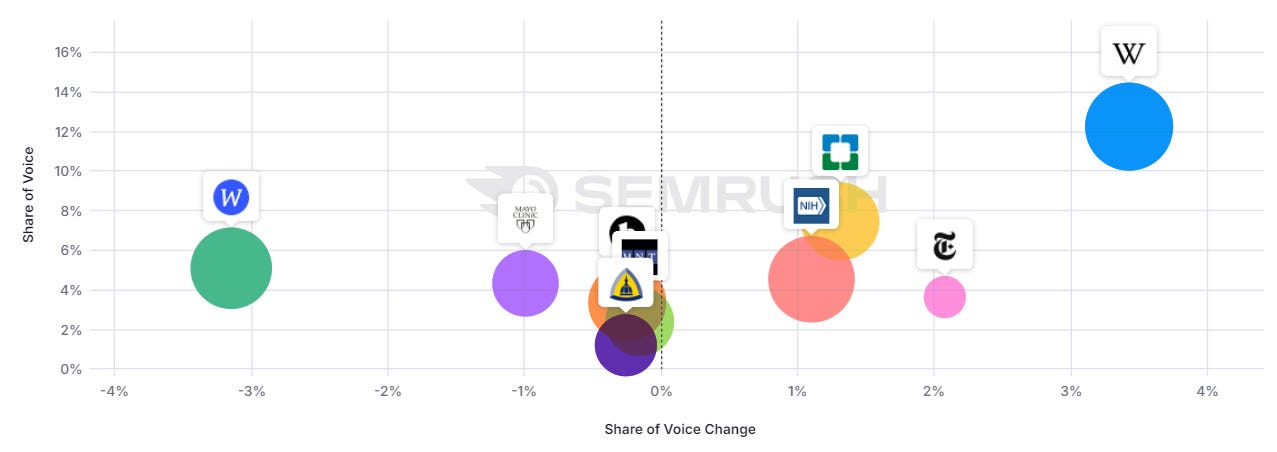

Picture Credit score: Kevin IndigWell being: combined image

Picture Credit score: Kevin Indig

Picture Credit score: Kevin IndigSaaS: extra manufacturers

Picture Credit score: Kevin Indig

Picture Credit score: Kevin IndigBe aware:

- This shift hit not simply shopper areas however B2B as properly.

- The influence in ecommerce is tougher to evaluate because of the dominance of free product listings.

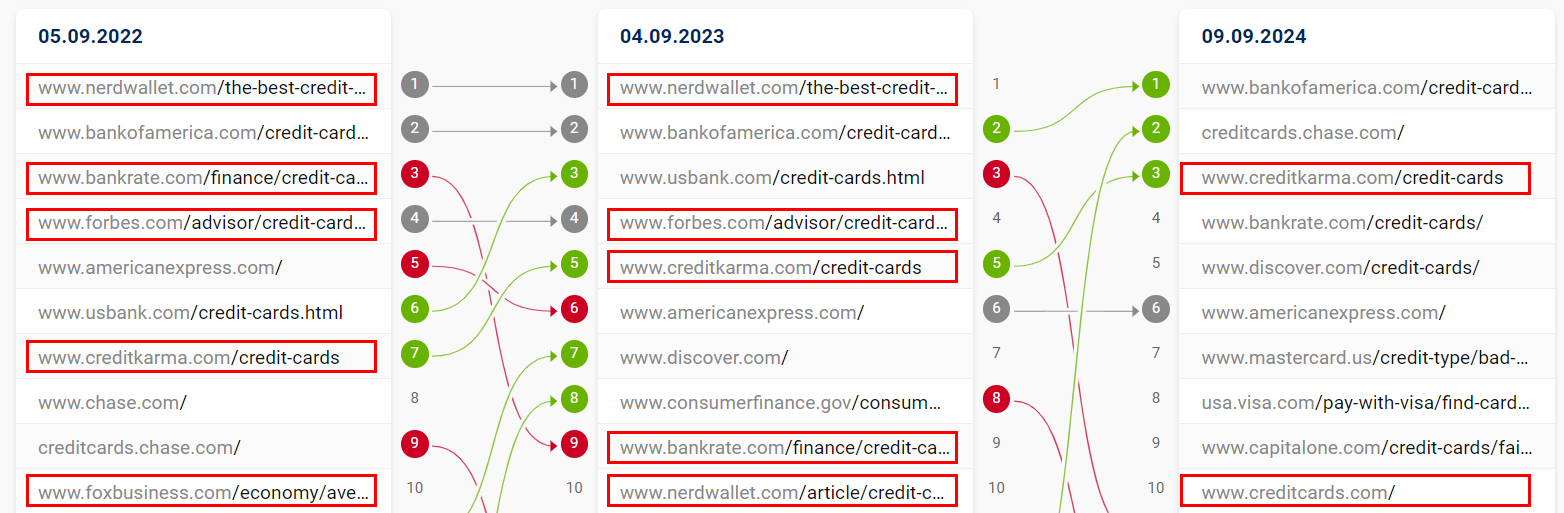

- In finance, main gamers like Nerdwallet misplaced quite a lot of visibility (there is perhaps extra occurring).

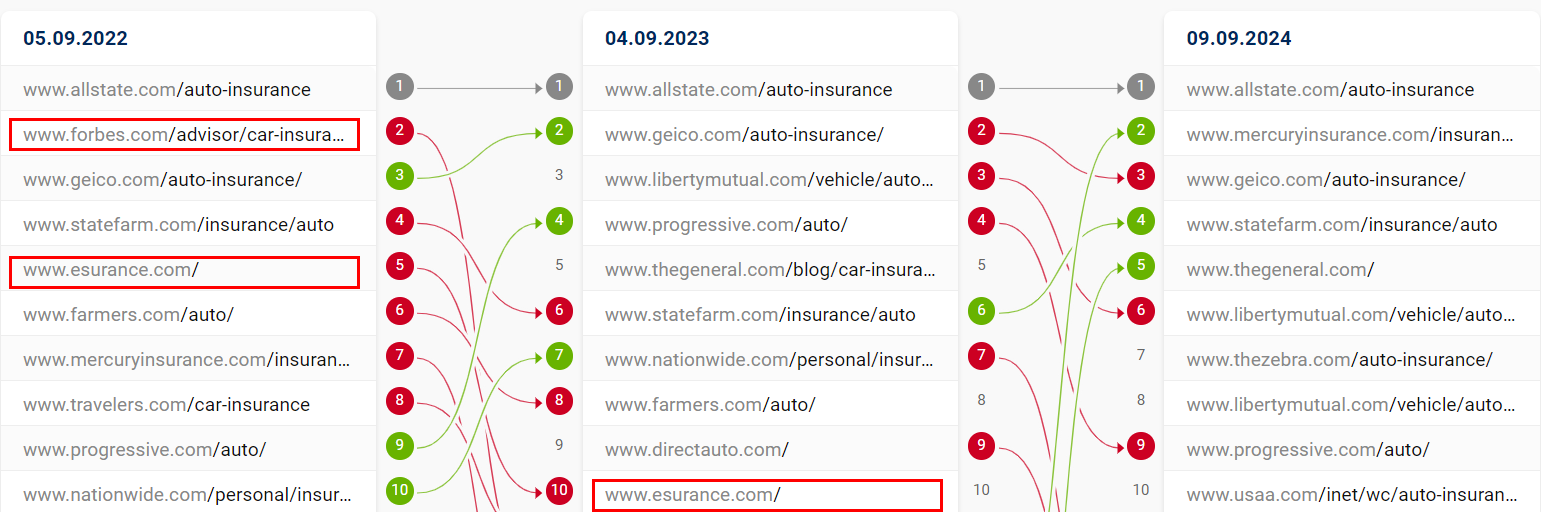

To high it off, three exemplary, hypercompetitive key phrases additionally present main SERP combine shifts over the past two years (non-brands highlighted in purple):

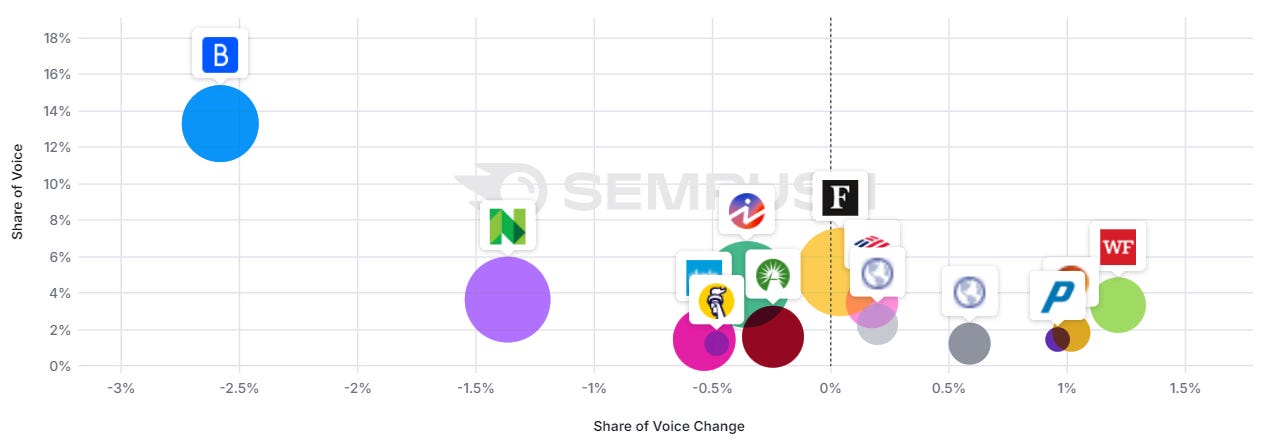

Credit score Playing cards: extra manufacturers

Picture Credit score: Kevin Indig

Picture Credit score: Kevin IndigAutomobile insurance coverage: extra manufacturers

Picture Credit score: Kevin Indig

Picture Credit score: Kevin IndigWatches: extra manufacturers

Picture Credit score: Kevin Indig

Picture Credit score: Kevin IndigResponse

Right here is how I work with firms that I don’t see as established manufacturers:

We work on status by mining critiques on third-party assessment websites and growing a plan for bettering them if obligatory.

Google strongly cares about third-party critiques (and so do customers), which you’ll see in the truth that it enriches the buying graph with them or cites them within the SERPs.

We put money into model advertising and marketing and monitor model recall/NPS in relation to rivals. We purpose all the time to be a little bit higher, which is an element of a bigger product technique.

In my expertise, web optimization and product should not separable. We monitor and put money into model mentions and in what context they’re talked about (co-occurrence).

We take into account laborious calls in the case of actual match domains (EMDs). Although you can see loads of examples that they work and the price of migration could be very excessive, generally shifting to a model title is the very best long-term possibility. What number of EMDs have you learnt which might be memorable?

We take a detailed have a look at the ratio of brand name to non-brand visitors – are each rising? When you have a low variety of branded searches in comparison with non-branded ones, you don’t have a model.

We have a look at model hyperlinks and mentions. Whereas generic anchor textual content hyperlinks are useful, folks are likely to underestimate the influence of brand name hyperlinks on the homepage.

The best belongings you usually do (within the white hat area) for extra model hyperlinks are additionally issues that get your model “on the map,” so this additionally funnels into a bigger model advertising and marketing technique.

Again in 2008, model hyperlinks have been seemingly the deciding model issue.

In the present day, it’s paired with model title searches, as Tom Capper’s evaluation on Moz reveals: domains that misplaced throughout Useful Content material Updates had a excessive ratio of Area Authority to Model Authority, which means numerous hyperlinks however few model hyperlinks.

The Helpful Content Update Was Not What You Think

Featured Picture: Paulo Bobita/Search Engine Journal